2024 LATAM SBC Report Coinchange

Acknowledgment

Thank you to our Co-authors & Contributors:

CryptoMarket with Fintech Association del Peru

Maria Fernanda Juppet Erwing, CEO at CryptoMarket for her review, feedback and content addition on the report, specifically regarding Brazil recent moves in cryptocurrencies. CryptoMarket is one of the largest cryptocurrency exchanges in the Latam area. In a constant process of growth, today it has a presence in Chile, Brazil, Argentina, Colombia and Peru.

CryptoMarket is a member of the FinTech Peru group that contributes to the economic development and growth of Peru. Fintech Peru focuses on working together by inviting private and public sector organizations to work on proposals to accelerate innovation through Fintech, promoting Fintech leadership within the country while integrating Latin America to the world, expanding the market size.

Borderless.xyz

Shane Hansen, Head of Operations at Borderless for his review and contributions to the report. Borderless.xyz is the infrastructure to transact globally with internet native money using stablecoins and RWAs. They empower builders to create efficient money movement, bring dollars to emerging markets needing stable currencies, and orchestrate the shift to on-chain banking.

M^0

Joao Reginatto, Chief Strategy Officer at M^0 and Nicole Schaefer, Senior Marketing Manager at M^0 for their feedback and contribution to the report. M^0 empowers builders of safe, programmable, interoperable stablecoins. By extending $M, a digital dollar building block issued by the M^0 protocol, developers can build branded, feature-rich digital dollars in minutes.

Bitso

Ingrid Carraro, Marketing Manager at Bitso Business and Christiana Cardoso, Head of Communications at Bitso Business and Gabriele Zuliani, Head of Revenue & Sales at Bitso Business for their feedback and review of the report. Bitso Business, with their blockchain-based payments platform empowers global businesses and customers to make and receive payments in local currency, and move money across borders effortlessly without prefunding.

El Dorado

Guillermo Goncalvez, CEO at El Dorado for their feedback and substantial contribution to the report, helping in its refinement. El Dorado is a stablecoins-powered Payments SuperApp for Latin America. Facilitating domestic and cross-border transactions, with connections to +70 local payment methods. El Dorado is transforming the way Latin Americans can access a dollar-based account that offers a stablecoin smart wallet, a P2P marketplace and gasless cross-border payments.

Mmerge

Paula Pascual, founder at Mmerge for the help in the promotional effort of the report to reach businesses in need of a stablecoin strategy in Latin America. At the core of Merge Madrid is a team of visionary thinkers, innovative creators, and blockchain enthusiasts, each bringing their unique expertise and passion to the table. Mmerge team is composed of experienced event managers, cutting-edge designers, strategic marketers, and industry-leading experts, all united by a shared commitment to pushing the boundaries of technology and creating unforgettable experiences.

BMB

Silvia Mogas, CEO and Founder at BMBWeb3 Ventures and Blockchain Marketing Boutique for the help in the promotional effort of the report to reach businesses in need of a stablecoin strategy. BMBWeb3 Ventures is composed of industry veterans in blockchain, AI, and emerging technologies. The firm delivers cutting-edge marketing and public relations strategies that help brands expand their reach, engage effectively with their audiences, and establish authority within the blockchain space. Silvia and her team are also instrumental in supporting companies with strategic initiatives such as stablecoin adoption, ensuring they resonate with the right business audiences and stakeholders.

Stablecoins Yield Generation: The Next Big Thing in LATAM

Stablecoins are emerging as a powerful tool in the world of finance. They're digital representations of traditional currencies often issued against U.S. dollars bank deposits. While the entire crypto market can be volatile, stablecoins offer a safer, more predictable option. They’ve grown quickly and represent perhaps the most impactful use case of crypto: today, the global stablecoin supply hovers around $200 billion. According to Coinbase's Q1 2024 report, stablecoins processed a record-breaking $30 trillion in transaction volume, solidifying their position as the killer app of crypto. More than just a store of value, they have become the backbone of fast, low-cost global payments, offering a practical alternative to outdated financial systems. With 36 million mobile wallets now actively using stablecoins, adoption is accelerating, bridging the gap between crypto and mainstream finance. (Coinbase)

Source: https://defillama.com/stablecoins

But why are stablecoins breaking into the mainstream and not just riding crypto market cycles? The answer lies in their ability to act as a truly global payment network—instant, programmable, and far cheaper than traditional methods. Major payment companies like Stripe and PayPal have taken notice. By lowering the cost of moving and storing value, stablecoins can create new revenue streams and reduce transaction fees.

In Latin America, stablecoins help consumers and businesses dollarize their savings, offering a safe haven to counteract inflationary processes that affect local currencies, which increases in markets where access to foreign currencies is restricted by legal authorities.

The Problem with Traditional Payments

Source: The Stablecoin Manifesto by Delphi Digital

Traditional payment systems involve multiple middlemen and fees at every step. Consider an average credit card payment:

• Merchants: Pay 2–3% in fees per transaction and wait 1–3 days for settlement.

• Payment Gateways: Charge monthly fees plus about 0.10% per transaction.

• Card Networks: Collect 0.05–0.15%.

• Payment Processors: Take 0.10–0.35%.

• Issuing Banks: Charge steep interchange fees (1.5–2.2%).

• Acquiring Banks: Add another 0.15–0.40%.

All these layers of fees and delays make transactions expensive and slow. Even giants like PayPal or companies like Starbucks have tried to sidestep these costs by creating their own closed-loop systems. Starbucks, for instance, encourages users to load money into their app, allowing them to process payments internally and even earn interest on the funds. While this reduces costs, it creates isolated “walled gardens” that don’t talk to each other—your PayPal balance isn’t compatible with your Starbucks account etc.

How Stablecoins Solve These Problems

Stablecoins run on open, decentralized ledgers, meaning they’re permissionless. Any merchant that accepts a given stablecoin can receive payments directly from consumers who hold the same stablecoin—no layers of middlemen. Another feature of these stablecoins is that they are interoperable. Regardless of the blockchain used by the user or the merchant, as long as the merchant accepts the stablecoin, a single stablecoin balance account can be used across countless merchants. The average cost of a stablecoin transaction is less than $1.

Stablecoin also provides a direct solution to unbanked people around the world. For the first time, creating a financial account is truly permissionless. No ID, no regulatory approvals—just an internet connection and a wallet and someone can receive payments.

In a high level overview, most users either send stablecoins for payment to a merchant directly using the blockchain (see arrows with 2, below), or they can send the payment via a fintech or payment gateway that the merchant uses as a services provider, simplifying their integration with the blockchain. The fintech will handle the communication and reporting from the blockchain on behalf of the merchant (see arrows with 1).

Source: Coinchange

This is why PayPal launched its own stablecoin, PYUSD: it aims to bypass traditional banking and card networks, cut costs, and offer instant settlement. With stablecoins, businesses anywhere can gain a global reach without the usual overhead. More recently Stripe acquired Bridge (for $1.1B!) which is a new payments platform built with stablecoins, specializing in making it easier for businesses to accept stablecoin payments without having to directly deal in digital tokens.

This path has been followed by several fintechs in Mexico, Argentina, and Brazil, which are developing stablecoin-based payment systems to incorporate this model into the local landscape.

As more companies discover the advantages of stablecoins—lower fees, simpler cross-border payments, and easy programmability—early adopters will gain a competitive edge. This game theory dynamic suggests that once some businesses integrate stablecoins, others risk losing out if they don’t follow suit. However, traditional banks may be slow to adopt stablecoins because it challenges their established revenue models. That leaves room for fintechs, neobanks, and other forward-thinking financial players to embrace stablecoins early and capture more value.

Neobanks, for example, can blend traditional and stablecoin accounts, offering customers faster settlement, lower fees, and even yield opportunities on their stablecoin balances. In traditional models, the yield from customer balances is typically captured by the sponsor bank, however by issuing stablecoins, the yield can be captured by the fintech. Wallet providers can earn extra revenue by sharing yield generated from lending stablecoins in decentralized finance (DeFi) markets. They benefit not only from the reduced payment costs but can also tap into new income streams like DeFi lending and liquidity provisioning.

LATAM: Leading the Way in Stablecoin Adoption

First let’s see why USD denominated stablecoins are such a big deal in Latin America (LATAM). Unstable local currencies, inflation, and limited banking access make stablecoins an essential financial tool. Their role in cross-border payments and remittances is growing rapidly, providing millions with a faster, cheaper, and more efficient way to move money. Unlike traditional remittance services that charge high fees and take days to process, stablecoins enable near-instant transactions, helping businesses and individuals transact globally without friction. (Coinbase)

For example, banks in Mexico cannot offer an account in USD to anyone who is not living within 20km of the US border. In Argentina, USD banking exists but they impose transaction volume thresholds, and the FX rate is unusually different (aka unfavourable) than the market rate. Local restrictions on foreign currency can prevent businesses to hold a USD balance, hence USD payments you receive are automatically converted into your local currency. This automatic conversion allows banks and remittance providers to easily add hidden fees by offering less favorable exchange rates. By allowing people to hold USD stablecoins, they can choose when to convert and clearly see the exchange rates. The same benefits apply to card payments. In countries with high cross-border taxes, like Brazil, stablecoins can also result in lower taxation than regular dollars. Some examples of fintechs operating in the stablecoin space for LATAM include Transfero, DollarApp, FelixPago and Bitso Business. Transfero focuses on integrating digital assets into traditional banking structures to streamline cross-border transactions, whereas DollarApp offers a user-friendly platform for everyday payments and savings in stablecoins. FelixPago specializes in facilitating instant remittances and payment services, and Bitso Business serves as a robust cross-border payments platform that connects users to both local fiat and crypto markets—together, these platforms highlight the diverse ways stablecoin technology is reshaping financial access and efficiency in Latin America.

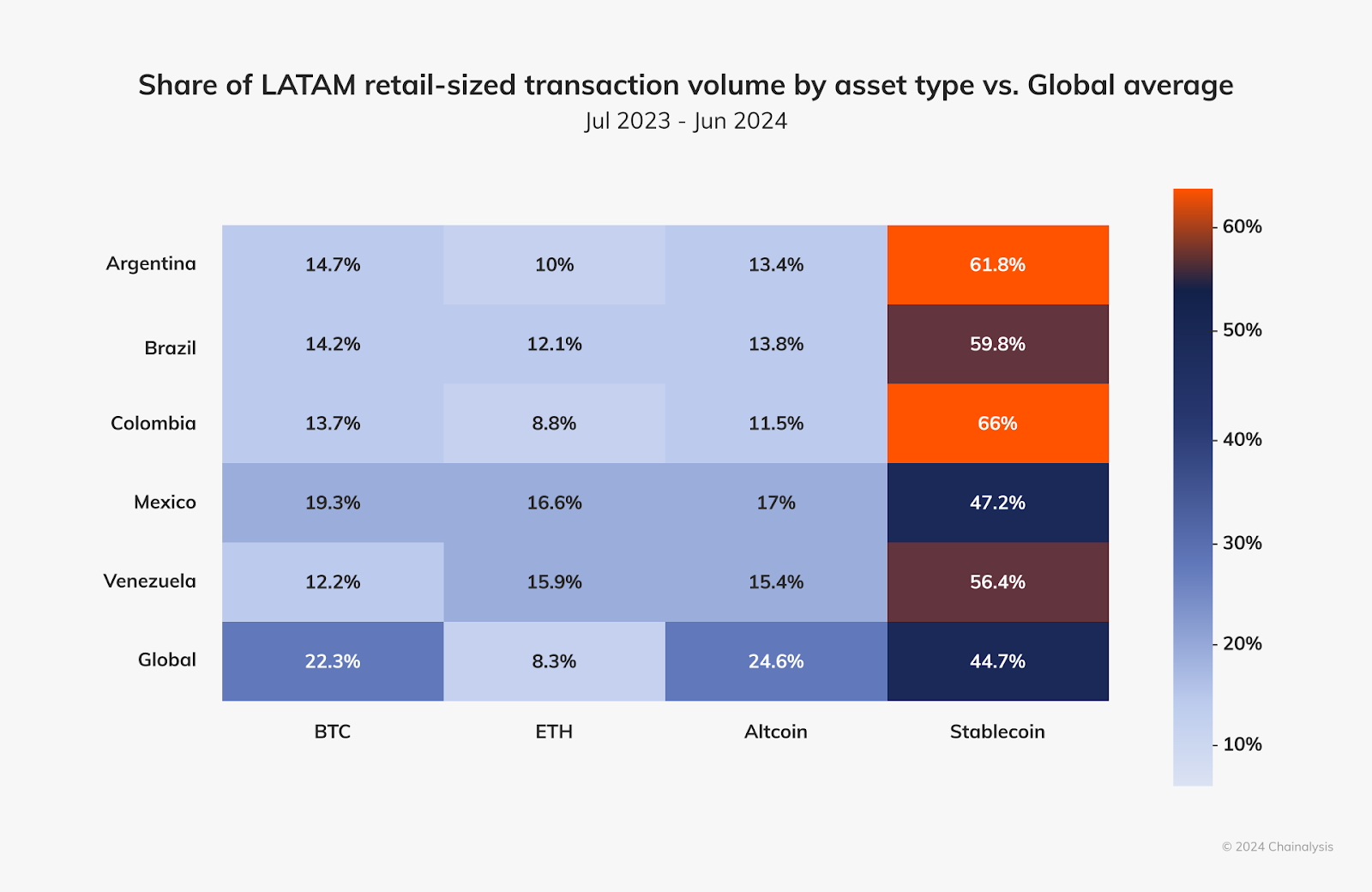

Here is a table that proves the level of growth of stablecoins in LATAM:

Source: 2024 Latin America Crypto Adoption by Chainalysis

According to a report from Bitso, a major crypto exchange in the region, both Bitcoin and stablecoins dominate user portfolios. In 2024, the use of USD stablecoins (USDC and USDT) expanded and accounted for 39% of purchases, representing growth compared to the 30% recorded in 2023. Users see them as a reliable tool for everyday transactions, remittances, and as a hedge against devaluation of their local currencies against the dollars, in countries such as Brazil and Mexico, and macroeconomic instability in Argentina and Colombia.

Source: 2024 Latin America Crypto Adoption by Chainalysis

According to Chainalysis, Latin America is the second fastest growing region with a year-over-year (YoY) growth rate of approximately 42.5%. If we look at the 2024 Global Adoption Index, of the top 20 countries, 4 are in Latin America: Brazil, Mexico, Venezuela, and Argentina.

Source: 2024 Latin America Crypto Adoption by Chainalysis

Around 70% of indirect flows from Brazil’s local exchanges to global exchanges now involve stablecoins. The country’s strong stablecoin usage and overall interest in digital services are attracting major players like Circle, which launched in Brazil in May 2024. Circle attributes its move to greater regulatory clarity and innovation-friendly policies. They’ve partnered with regional businesses to offer fast, low-cost, around-the-clock access to USDC, and are expanding their local footprint. All in all, profound changes are expected in the ecosystem of crypto exchanges in Brazil in 2025, given the new regulatory requirements to have the “crypto license”, which require they keep funds of up to USD $1.2M in the country as collateral for their local clients in case of defaults. As a result, the number of people using USDC in the region is expected to grow rapidly. This situation should be further enhanced by increasing the degree of local protection for consumers.

Another interesting chart is the correlation between the value of Argentine Peso (ARS) and the stablecoin trading volume on one of their exchanges:

Source: 2024 Latin America Crypto Adoption by Chainalysis

Argentina’s long struggle with inflation and the peso’s steady decline has pushed many to find alternatives. By late 2023, inflation reached 143%, nearly 40% of the population lived in poverty, and the new president devalued the peso by 50%. In response, people turned to black market U.S. dollars and USD-pegged stablecoins. Data from Bitso shows that each time the peso weakened, stablecoin trading surged—from over $1 million when the peso fell below $0.004 in July 2023, to over $10 million after it dipped below $0.002 in December 2023. As a result, stablecoins now make up 61.8% of Argentina’s crypto transaction volume—one of the highest in Latin America. Venezuela has a similar chart below:

Source: Federal Reserve and Chainalysis

“In addition to retail adoption of stablecoins, we’ve seen a surge of demand from corporates with subsidiaries in LATAM” says Kevin Lehtiniitty, CEO of global stablecoin orchestration network Borderless.xyz. “In a high currency volatility environment, these companies pay high FX fees to lock in rates or are subjected to significant FX risk from the rate changing over a one or more day long settlement cycle. By leveraging stablecoins, they can make these cross-border transfers instantly, dramatically reducing the FX risks and associated costs.”

LATAM stands out as a prime region for stablecoin growth. Countries here have faced economic volatility, high inflation, and frequent currency devaluations. Stablecoins linked to stronger currencies, like the U.S. dollar, provide a stable store of value. They also offer faster, cheaper ways to send and receive money—crucial in a region where remittance costs are notoriously high.

- Argentina: From young to old generations, they increasingly turn to stablecoins to protect their savings against inflation.

- Brazil: Many businesses accept stablecoin payments for cross-border transactions.

- Mexico: With a strong remittance market, stablecoins are becoming a powerful tool for quick, cost-effective money transfers.

Regulations are evolving, and as stablecoins gain trust and familiarity, adoption is likely to surge. They bring stability and efficiency that align with the everyday financial needs of people in LATAM.

Venezuela: A Prime Example For Stablecoin Adoption

Venezuela, for example, has faced one of the most severe economic crises in the region, characterized by hyperinflation that reached alarming levels, with a rate exceeding 65,000% in 2018 (Statista). This situation has eroded the purchasing power of citizens and generated widespread distrust in the local currency, the bolívar. Additionally, government-imposed exchange controls have made access to foreign currencies difficult, limiting the ability to save and protect against devaluation.

In this context, stablecoins—cryptocurrencies pegged to the value of strong currencies like the U.S. dollar—have emerged as an effective solution to mitigate the effects of inflation and economic instability. Guillermo Goncalvez, CEO and founder of El Dorado, has highlighted that Venezuela has become "the world capital of stablecoins and its main use case," due to the widespread adoption of these dollar-pegged tokens (News Bitcoin). Venezuelans use stablecoins such as USDT and USDC to protect their savings from hyperinflation and conduct daily transactions more securely and stably.

In an article published in Forbes, Goncalvez described stablecoins as "oracles in times of darkness," emphasizing their crucial role in economies affected by instability. According to data from the analytics firm Chainalysis, Venezuela ranked third globally in cryptocurrency adoption in 2020, with a significant portion attributed to the use of stablecoins. This phenomenon has enabled citizens to safeguard their savings and conduct transactions more reliably amid economic and political crises.

The adoption of stablecoins in Venezuela has also facilitated remittances, allowing millions of Venezuelans abroad to send money to their families more efficiently and at lower costs. Goncalvez notes that this trend has intensified during periods of political and economic uncertainty, making stablecoins a crucial tool for those sending money home (Bitget). This phenomenon has positioned Venezuela as a model of global financial resilience, demonstrating how cryptocurrencies can provide effective solutions in economies affected by instability and inflation.

This illustrates how stablecoins are revolutionizing the financial landscape in Latin America, offering solutions to traditional economic challenges and fostering financial inclusion in the region. Beyond serving as a hedge against inflation, they are driving a new era of digital payments, international trade, and access to decentralized financial services. As Goncalvez stated in Forbes, "Stablecoins have proven to be beacons of stability in emerging markets where uncertainty reigns”.

Regulation and Education: A Path to the Evolution and Mass Adoption of Stablecoins

Latin America continues to attract increasing levels of international investment with its expanding business opportunities and dynamic entrepreneurial landscape. According to the Bitso Business study, conducted by PCMI, "From Barriers to Bridges: How Blockchain Can Reshape Cross-Border Payments in Latin America”, the region has emerged as the fastest-growing remittance market, with the B2B cross-border payments sector expected to more than double, rising from $600 billion to $1.37 trillion by 2030.

Despite these growing opportunities, companies face significant challenges when expanding into Latin American markets. On the payments front, many businesses encounter inefficiencies, inadequate infrastructure, and unnecessary costs due to fragmented and incompatible banking systems around the world that make global payments an expensive, slow, and inefficient process. Additional key local obstacles include technological infrastructure, regulatory compliance, security, fraud prevention, and financial inclusion.

The research identifies the main barriers companies face with cross-border payments and analyzes how blockchain technology and stablecoins, by removing intermediaries, are rapidly emerging as an alternative to move money in a faster, cost-efficient, and transparent way.

Two current challenges that need to be overcome refers to regulation and education. Although we still find diverse and inconsistent regulation scenarios across the region, countries like Brazil are advancing on the regulatory clarity, conducting a collaborative regulatory process concerning stablecoins, which contributes to this asset class gaining more market share and institutional security.

Regarding education, industry leaders have been working with institutions and the broad community to overcome skepticism regarding the full potential of blockchain for business. As stablecoins’ advantages become more widely acknowledged across different industries, we expect to experience a substantial increase in its application in cross-border payments, transforming how 21st-century companies move money and expand their business across the globe.

Stablecoin Yield: A New Value Proposition

Beyond payments, stablecoins offer yield opportunities. Fintechs and neobanks can offer their customers interest-bearing stablecoin accounts, attracting new users and retaining existing ones while unlocking new revenue streams. These yields, in the range of 10%-30%, come from lending stablecoins in DeFi markets or providing liquidity using complex DeFi strategies which Coinchange offers through the infrastructure that other fintechs can integrate with. You might ask why can’t we do it on our own? Why do we need Coinchange? While building a "yield on stablecoins" feature in-house is theoretically possible, there are lots of technical complexities involved. Integrating with various DeFi protocols requires deep technical expertise in blockchain development and smart contract interactions (Coinchange does not use publicly available UI, which eliminates several UI related risks). Real-time monitoring of DeFi protocols is another tedious task. Continuously monitoring the performance of these protocols and adjusting strategies to optimize yield while minimizing risk is resource-intensive. We have experienced all sorts of market cycles since we started building in 2018 and it takes tremendous risk-monitoring and mitigation to strike a balance between high yield and building DeFi strategies.

Then there is a regulatory hurdle that needs to be overcome in terms of obtaining necessary licenses and certifications for financial services, which can be a lengthy and costly process. Partnering with a specialized yield infrastructure provider who has deep expertise in DeFi protocols, risk management, and regulatory compliance, can help you integrate and scale much faster.

What’s Your Stablecoin Strategy?

We haven’t even explored the intersection of stablecoins and AI agents which is a unique combination of native digital currencies and a smart digital algorithm to execute tasks in the real world. That’s a topic for another blog but nevertheless something that could explode the usage and adoption of stablecoins. The stablecoin revolution is not just hype—it’s here, and it’s reshaping how we think about money, payments, and financial services. Forward-thinking fintechs and wallet providers can seize this opportunity to lower costs, improve margins, and open new revenue streams through stablecoin yields.

All of a sudden, everyone is expected to have a stablecoin strategy. For many, especially for payment service providers and financial institutions, the question to be answered is why should I integrate stablecoins, and if so how?. At the end of the day, integrating with stablecoin rails can mean offering customers faster, cheaper global transfers, as well as some benefit from yield on underlying reserves.

However, one critical angle many companies might be missing when they think of their stablecoin strategy is whether they should build their own stablecoin or adopt an existing one. Projects such as M^0 allow any business to quickly build their own stablecoin. But why would someone be interested in that, and isn’t it too complicated a strategy? Interestingly enough, this might be the right path for a large number of businesses. If you are an app or a service that accumulates digital dollar deposits from end users, storing those funds in the form of your own stablecoin not only gives you access to income from the yield on reserves, but also gives you greater control over your financial stack and its future ( compared to relying on a third-party stablecoin). Technology is advancing fast in the stablecoin space, and networks like M^0 are well positioned to lead the way of the enterprise adoption of stablecoin, benefiting from yield on reserves, while maintaining interoperability and unified liquidity.

For businesses, the question isn’t if stablecoins will go mainstream—it’s whether you’ll lead the charge or risk falling behind. With the right partnerships and infrastructure, you could integrate stablecoin payments and yield features in under a week. The benefits are too significant to ignore: stable value storage, faster cross-border payments, reduced fees, and a clear path to earning yield on idle balances.

In a world where financial innovation is accelerating, stablecoins stand out as a practical, accessible tool that can boost your bottom line and help you stay ahead of the competition. The future of money is digital, and stablecoins are key to unlocking it. So, what’s your stablecoin strategy? Don’t have one? Contact us

Latest articles

Coinchange Financials, Inc.

261-250 University Avenue

Toronto, Ontario M5H 3E5 CANADA

Coinchange Financials Inc.

Corporation Trust Center 1209

Orange St.Wilmington,

DE 19801 USA

Coinchange Financials SP. Z.O.O.

Grzybowska 80/82/700

00-844 Warszawa, Poland

Note: Crypto assets are not legal tender, are not backed by the government, and crypto accounts held with Coinchange are not subject to FDIC or SIPC protections. The value of crypto assets are not static and can fluctuate substantially. Not all products and services are available in all geographic areas and are subject to Coinchange’s applicable terms and conditions. Eligibility for particular products and services is subject to final determination by Coinchange. Rates for our products are subject to change. Nothing on this website should be construed as a recommendation for any action. Coinchange is registered as a Money Services Business (MSB) number 31000304503627 with the US Financial Crimes Enforcement Network (FinCEN).